EB-5 Source of Funds: A Practical Guide for Indian and Chinese Investors

A step-by-step guide to documenting lawful source of funds for EB-5 petitions, with specific notes for investors from India, China, and other high-volume sending countries.

Why source of funds is the biggest single cause of EB-5 delays

If you ask a USCIS adjudicator what kills an I-526E petition, they will tell you it is almost never the project. Regional Center compliance, TEA designation, job-creation math — these things are visible on the first page of a memorandum, and by the time they reach an officer's desk they have usually been vetted ten ways. What kills petitions, over and over again, is source of funds. The capital trail. The documentary chain that has to carry the money from the lawful economic activity that generated it, through the bank accounts and currency conversions that moved it, all the way to the escrow account of a United States Regional Center — without a single missing link.

A Request for Evidence, or RFE, on source of funds is the single most common way an EB-5 petition gets delayed by six to eighteen months. An RFE is not a denial; it is an officer telling you, in formal language, that the evidence in your petition does not fully satisfy the preponderance-of-evidence standard. The remedy is more paper. But more paper, assembled in a foreign country, often in a foreign language, frequently from decades-old transactions, is the part of this process that separates petitions that close cleanly from petitions that stall.

This post is a practitioner's walkthrough. It is not legal advice and it is not a substitute for qualified immigration counsel. It is the set of questions we ask every prospective EB-5 investor before a petition is filed, and the documentary posture that makes adjudication go smoothly.

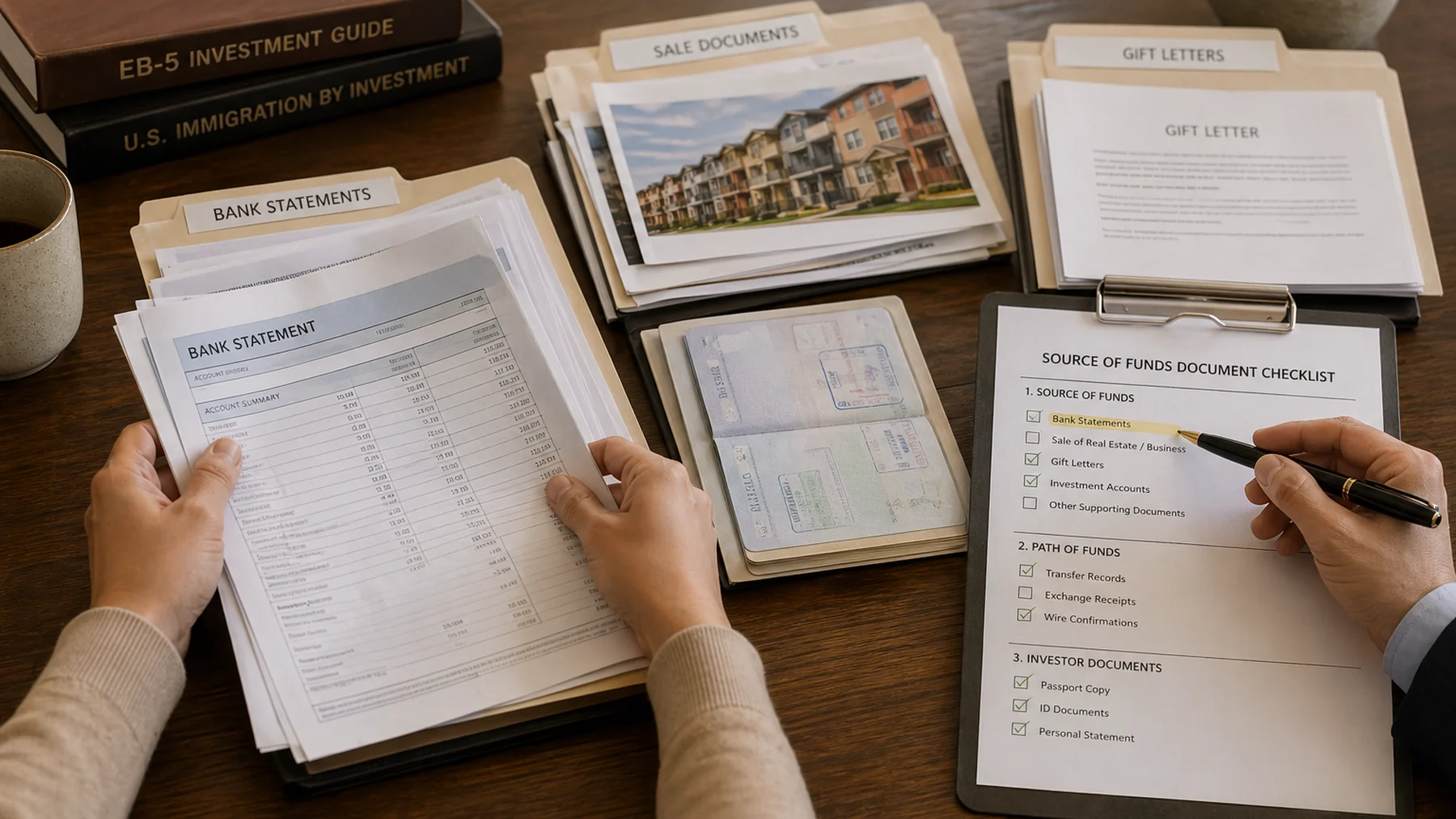

The two documents every petition needs, regardless of path

No matter which source-of-funds path you take, two things have to be in the record. First, a source-of-funds narrative: a written, signed statement from the investor, usually prepared with counsel, that walks the officer through the story of the capital. "In 2011, I sold my share of a manufacturing business in Pune. The proceeds were deposited in my ICICI Bank account. In 2013, I used those proceeds to purchase commercial real estate. In 2022, I sold that real estate for a gain of X rupees. That gain, after capital gains tax paid to the Income Tax Department, is the capital now being invested." The narrative is the spine.

Second, a path of funds: the bank-by-bank, wire-by-wire trail that shows the money actually moving from the lawful source to the US escrow account. This includes every intermediary account, every currency conversion, and every foreign-exchange remittance. In India, this will involve an Authorised Dealer (AD) Category-I bank and a Liberalised Remittance Scheme (LRS) declaration under the Reserve Bank of India. In China, this will involve the foreign-exchange quota administered by the State Administration of Foreign Exchange (SAFE), along with the mechanics that have made Chinese EB-5 capital such a complex compliance story for twenty years.

A petition without both the narrative and the path is, in most cases, not ready to file.

USCIS does not penalize you for having a complicated story. It penalizes you for leaving a gap. A detailed narrative with ten bank statements beats a clean summary with three.

Path 1 — Salary and savings

The most straightforward source-of-funds path is also the rarest for EB-5 capital at the current $800,000 TEA minimum. Accumulating $800,000 of post-tax savings from salary alone requires a very senior career arc, typically over fifteen to twenty-five years. For the executives and senior physicians who do take this path, the documentary package is clean: tax returns for every year in which income was earned (the US standard is usually five years of returns, though for deep history ten is sometimes helpful), employment contracts or offer letters showing salary progression, pay slips, and bank statements showing the deposits accumulating.

The analytical work is matching. Officer wants to see that the salary line on the tax return roughly matches the deposits on the bank statement, that the ending balance each year grew in a way consistent with stated savings, and that the final $800,000 plus administrative fees came from an account that, on its face, grew from employment income rather than from a large unexplained deposit. An account that sat at $40,000 for six years and jumped to $900,000 three months before filing tells a story that needs more documents — not a refusal, just more documents.

Path 2 — Business ownership and dividends

The business-ownership path is the most common for EB-5 investors from India, China, and most emerging-market sending countries. The investor owns some or all of an operating business, the business generates profits, profits are distributed as dividends, and the dividends are the capital used for EB-5. On paper this is simple. In practice, each step requires its own documentary block.

For the business itself: incorporation documents, ownership certificates, audited financial statements for the past three to five years (or unaudited statements prepared by a chartered accountant where audits are not statutorily required — a common pattern for Indian private limited companies below certain thresholds), tax returns filed with the relevant national tax authority, and evidence of the business's operational reality (office lease, employee rolls, major customer contracts, industry licenses). USCIS wants to see that the business actually exists and generates real revenue, not just that a company name exists on a registry.

For the dividends: board resolutions authorizing dividend distributions, bank statements of the business showing the dividends paid out, and bank statements of the investor showing the dividends received. If dividends were paid to the investor over many years and accumulated before being used for EB-5, the accumulating balance needs to reconcile. If dividends were paid in the local currency and later converted to dollars, every conversion step needs its own wire trail and its own declaration under the relevant foreign-exchange regime.

For Indian business owners: the LRS limit is $250,000 per financial year per individual. An $800,000 investment therefore requires, at a minimum, funds drawn from multiple family members' LRS quotas across multiple financial years — or a single investor saving LRS remittances across four financial years. This is mechanically achievable but needs to be planned twelve to thirty-six months in advance. For Chinese business owners, the SAFE annual limit per individual is $50,000, which historically meant that EB-5 capital from Chinese investors has relied on family pooling, pre-positioned offshore accounts, or legitimate business-related currency channels — all of which are permissible with the right structure, but each requires its own documentary discipline.

Path 3 — Real estate sale

The real-estate-sale path is the second most common for EB-5 investors globally. The investor acquires a property, holds it for some period, sells it, pays capital gains tax, and uses the after-tax proceeds for EB-5.

The document set is specific. For the acquisition: the sale deed (in India, the registered conveyance deed; in China, the property ownership certificate), evidence of the purchase price paid, and evidence of the source of the original acquisition capital — because the path-of-funds requirement flows backward through every significant transaction. If you bought a property in 2005 and are selling it in 2025 to fund EB-5, USCIS may want to see where the 2005 acquisition capital came from. This is the recursion that catches many investors off guard.

For the sale itself: the sale deed or equivalent, bank statements showing receipt of the sale proceeds in the investor's account, the capital-gains tax computation and proof of tax paid, and — in India — the Tax Deducted at Source (TDS) certificate from the buyer, which is statutorily withheld on real estate transactions above certain thresholds. Officers look for the math to match: sale price minus acquisition cost minus statutory deductions equals the declared capital gain; capital gain multiplied by the applicable tax rate equals the tax paid; sale price minus tax equals the net proceeds available for remittance.

The real-estate-sale path is clean when the holding period is long and the tax paperwork is complete. It is messy when the acquisition capital itself is undocumented — a common issue for pre-2000 property purchases in India and China.

Path 4 — Gift from a family member

Gifts are common — especially in Indian EB-5 petitions, where adult children frequently receive gifts from parents who accumulated capital over a business career. Gifts are also the source-of-funds path that attracts the most USCIS scrutiny, because a gift has to be a gift, and the capital being gifted still has to be demonstrably lawful.

The gift path requires, at minimum: a signed gift deed or gift affidavit that irrevocably transfers the funds from the donor to the recipient with no strings attached (meaning no loan, no expectation of repayment, no encumbrance), evidence of the donor's own lawful source of the gifted capital (so the donor in effect has to complete a parallel source-of-funds package), evidence of the transfer itself (bank statements on both sides), and in many cases an explanation of the donor-recipient relationship sufficient to make the gift credible on its face.

In India, the Income Tax Act exempts gifts between certain specified relatives (parent, child, sibling, spouse) from gift-tax treatment; gifts from non-relatives above a certain threshold are taxable to the recipient. Documenting that a gift was between specified relatives is usually straightforward. Documenting that the donor's capital was lawful is where most RFEs originate. If your father is gifting you $600,000, and your father's capital came from a family business, then your father's business needs the same documentary treatment as if he were himself the EB-5 investor.

Path 5 — Inheritance

Inheritance is a cleaner story than gifting, because inheritance implies a legal event (the death of the decedent) that is independently documented. The document set: the death certificate of the decedent, the probated will or equivalent succession document, the succession certificate or letter of administration that legally transfers title, bank or asset statements showing the inherited capital, and — as with gifts — evidence of the decedent's lawful accumulation of that capital during their lifetime. The "lawful accumulation" requirement is where some investors run into difficulty, especially when the decedent died decades ago and original records are incomplete.

Country-specific notes

India. The Indian EB-5 investor base has grown rapidly since 2019, driven by backlogs in the employment-based green card categories (EB-2 and EB-3) for India-born nationals. The relevant regulatory regimes are the Reserve Bank of India's Liberalised Remittance Scheme ($250,000 per individual per fiscal year), the Income Tax Act (for dividend, capital-gains, and gift treatment), and the Foreign Exchange Management Act (for the remittance mechanics). Most Indian EB-5 petitions draw on family business dividends or real-estate sales. Chartered accountant (CA) certificates — specifically, Form 15CA and Form 15CB under the Income Tax Act — are often central to the remittance documentation. Engage your CA early; they will coordinate with your bank on the outbound remittance paperwork and their certificate becomes part of the USCIS file.

China. The Chinese EB-5 investor base was the dominant source of EB-5 capital from approximately 2010 to 2018. Visa backlogs in the China-born category lengthened wait times substantially, which combined with broader China policy shifts and the 2022 Reform and Integrity Act has reshaped the flow. The mechanics: SAFE administers a $50,000 per individual per year outbound foreign-exchange quota. Legitimate family pooling across multiple relatives is the long-established compliance path; the documentary requirement is that every pooled contribution can independently prove lawful source and that no contributor is acting as a nominee for someone else. Chinese tax documentation, business licenses, and property ownership certificates are now widely accepted by USCIS when properly translated and apostilled.

Vietnam. Vietnam has emerged as a significant EB-5 source country since roughly 2016. The State Bank of Vietnam regulates outbound currency flows, and most Vietnamese EB-5 investors use business-ownership or real-estate-sale paths. Documentation is typically available but less standardized than in India or China; an experienced Vietnamese accountant who has assembled EB-5 packages before is a meaningful advantage.

South Korea. Korean EB-5 investors often draw on business sale proceeds or long-held real estate. The Bank of Korea's overseas investment regime is relatively permissive by regional standards. Korean tax records are well-organized and translate cleanly; the complications, when they arise, tend to be around family-entity ownership structures that USCIS wants mapped before it will credit the ultimate source.

Working with a qualified CPA and immigration attorney

The single best decision an EB-5 investor makes is not which Regional Center to invest with. It is which two professionals to engage. The first is a qualified immigration attorney who has filed I-526E petitions for nationals of your country before — not merely a generalist immigration lawyer. Country-specific document conventions matter. The second is a CPA (or, in India, a Chartered Accountant; in China, a registered public accountant) who can produce the tax-and-remittance paperwork in a form an American immigration officer can read and cross-reference to your bank statements.

These two professionals typically charge between $20,000 and $60,000 combined for an EB-5 source-of-funds package and petition, depending on complexity. That fee is less than the cost of a single RFE delay measured in opportunity cost, and it is far less than the cost of a denial. Treat this fee as part of the $800,000 investment, not as an optional extra.

What we ask before we accept an EB-5 subscription

Before we will accept an EB-5 subscription into one of our Regional Center offerings, we ask the investor to confirm three things. First, that they have retained qualified immigration counsel and that counsel has reviewed the project's offering documents. Second, that their source-of-funds package is in draft form — meaning the investor, with counsel and accountant, has identified the capital path, assembled the documentary set, and has a clear view of what will be in the petition. Third, that the investor understands the process timeline (realistic I-526E adjudication is 18 to 36 months today, conditional green card issuance follows adjudication, and the unconditional green card requires an I-829 petition approximately two years later) and is making a multi-year commitment with that timeline fully in view.

None of this is legal advice. It is how we try to make sure that the EB-5 investors who come into our projects have the best chance of a clean petition and a meaningful outcome. The program, properly used, is one of the few remaining direct paths to US permanent residency for a family that is prepared to commit capital, commit time, and commit to full documentary transparency. The investors who treat it as a mechanical process — "wire the money, fill out the form" — are the ones who get hurt.

For an overview of how our projects fit into this pathway, see our EB-5 page; for the broader firm and how EB-5 sits alongside our other vehicles, our investment overview is the natural second read.

Related

EB-5 vs E-2 Visa: Which Is Right for Your Family in 2026?

How to Verify Accredited Investor Status: A Rule 506(c) Walkthrough

Qualified Opportunity Zones: A Bay Area Investor's Guide to 2026

Explore our EB-5 offering and investor pathway.

Bay Area and Central Valley projects structured for EB-5 investors with appropriate TEA and job-creation profiles. Documentation and project memoranda available to investors with counsel engaged.